NVIDIA Through a Crypto Miner's Eyes

For the past two years, watching people scramble for NVIDIA cards and the AI frenzy run hotter every quarter, I keep getting a strange flicker of recognition. I’ve seen this before. Roughly ten years ago, through my own stint as a miner, I lived the whole arc once.

I’m not here to analyze NVIDIA. I want to talk about a few things those mining years left me — and the lens they hand me for looking at the world’s most valuable company.

Up front: this is personal observation, not investment advice.

Let me start with my rigs. I’ll keep it short — it’s only the setup.

The Setup: My Mining Rigs

At the peak of the 2017 ETH mining craze, GPUs weren’t just expensive — they were gone. China was still the world’s crypto mining capital back then, and every mining-capable card got swept up domestically first. I bought over twenty cards, mostly NVIDIA, a few AMD. Some I fought for locally; others I ordered from the UK through Amazon, shipped in batches over weeks. The last batch spent a month on a cargo ship before reaching Shanghai. Once I had them all, I assembled six-card rigs, set them up in my attic, and let them hum. A big standing fan pointed at them. In summer, I ran the air conditioning too. Electricity ran several thousand RMB a month. Sometimes the house circuit couldn’t handle it — tripped the breaker more than once.

I put up with all of it because the money was genuinely good.

I stopped because of the late-2018 ETH crash. As Ethereum’s price kept falling, there came a point where what I mined couldn’t even cover the power bill. Mining rigs aren’t like stocks — if a stock drops, you can hold and wait, it costs you nothing. A mining rig burns real money every single day it’s running. The moment revenue dips below cost, your money-making asset becomes a hole that bleeds cash. So I shut them down.

I never sold a single one of those twenty-plus cards. Anyone in the GPU world knows mining cards are untouchable — running 24/7 destroys the VRAM, and nobody wants them. They sat in my attic for years until I moved house and finally scrapped them. From hunting them down across the globe to disposing of them as junk — about seven years.

That’s the setup. I dwell on it because the GPUs that ate my power bill back then were mostly NVIDIA’s — and the GPUs eating the world’s data-center power today are still NVIDIA’s. Nearly a decade apart, same protagonist; only the label changed, from “gaming” to “AI.” Those years handed me a pair of glasses: with any capital-heavy asset, ask a few questions before anything else. Below, I aim those questions at NVIDIA.

How Much of the Demand Is Real?

NVIDIA’s quarterly earnings are staggering right now — each one better than the last. But impressive earnings and real demand have never been the same thing. The mining boom taught me that.

During that scramble, how many buyers were real gamers, and how many were miners like me? This isn’t hindsight. A big slice of NVIDIA’s revenue in those years was actually mining money — booked under gaming, and counted as genuine growth in gaming demand. In 2022 the SEC found that NVIDIA had failed to tell investors mining was a “significant” reason its gaming revenue surged across several quarters of fiscal 2018, and the company settled with a fine. A class action is still grinding on, alleging more than a billion dollars in mining-related sales were buried inside “gaming.” Then the mining crash hit, that demand evaporated overnight, and the earnings were exposed for what they were: inventory piled up, the stock halved. Demand that looked bottomless had a huge chunk that could vanish in an instant — and at the time almost no one, NVIDIA included, was willing to mark it off on its own.

Today’s AI compute demand is the same setup. How much of it comes from applications that actually make money, and how much is pure arms race — “everyone else is buying, so I can’t afford not to”? On the books, both kinds look identical. You can only tell them apart after the tide goes out. And right now, a hard-to-ignore fact: end-user revenue across the entire AI industry is still in the tens of billions per year, while the big tech companies’ combined capital expenditure is heading toward $700 billion in 2026 and projected to break $1 trillion in 2027. Sequoia Capital did the math back in 2024: to justify spending at that scale, the industry needs $600 billion in annual revenue. Actual revenue is nowhere close. The enormous gap in between is held up by one thing — the not-yet-proven expectation that “AI will change the world.”

Versatility: Moat and Achilles’ Heel

When I was getting into mining, a friend advised me: buy GPUs — they’re insurance. If ETH goes south, you can mine other coins. Worst case, you can game on them. Sounded reasonable. Versatility. If one road closes, there’s always another. That’s the biggest seduction of a general-purpose tool: it makes you feel like you’ve kept a fallback open.

But crypto mining’s history drew a very precise boundary around that “fallback.”

Start with Bitcoin. BTC’s algorithm is extremely friendly to specialized chips (ASICs). Once ASICs arrived, GPUs got crushed — orders of magnitude difference. Same kilowatt-hour, but a dedicated mining machine produced hundreds to thousands of times more hashpower. GPUs were instantly unviable for BTC. Entire fleets got pushed out.

Ethereum was different. ETH’s algorithm was deliberately designed to be memory-hard — specifically to resist ASICs. Result: even when ETH-specific mining machines eventually appeared, the memory bandwidth bottleneck kept their edge over GPUs modest. Not an order-of-magnitude gap. So GPUs survived on the ETH track — barely.

Put the two threads together and you get the real origin of the 2017 ETH boom: GPU miners, driven out of Bitcoin by ASICs, poured into ETH — the one algorithm ASICs couldn’t crack. The refuge I ran into was itself a refugee crisis, made by an earlier round of “specialized crushing general-purpose.” My friend’s “you can always mine something else” did keep GPUs alive for a while — not because versatility is dependable, but because ETH’s algorithm happened to shrug ASICs off. Whether a fallback exists was never my call. It belonged to the other side’s chip, and to the algorithm.

And once specialization is proven viable in a domain, it spreads and iterates terrifyingly fast. The moment an algorithm is shown to be ASIC-able, dedicated machines flood the market. They start on cheap mature process nodes to prove the concept, then sprint toward faster, more power-efficient versions — each generation more ruthless. “It’s not strong enough yet” is never a reason for comfort. It’s weak now precisely because it just started.

Now put that lens on NVIDIA.

NVIDIA’s cards are valuable precisely because they can compute anything. But over the past two years, AI’s center of gravity has been shifting from training to inference. You train a model once; after that, it gets called for inference by hundreds of millions of users, countless times a day. The two demand curves aren’t symmetric: training compute will eventually plateau as models grow and training cadence stabilizes. Inference is different — it scales with users. More users, more calls, no ceiling. Inference will inevitably overtake training as the bulk of AI compute.

Inference is high-volume, repetitive, algorithm-fixed — exactly the scenario where specialized chips excel and general-purpose GPUs are at their weakest. So Google’s TPUs, Amazon, Microsoft, Meta — NVIDIA’s biggest customers — are all building chips purpose-built for inference.

NVIDIA currently holds roughly 85–90% of the AI chip market. But that number hides a structural detail: it’s above 90% in training, only 60–70% in inference. Multiple analysts project its overall share could fall from ~90% to ~70% within two or three years, with inference being where the ground is lost. Custom chip shipment growth this year is nearly 3x that of general-purpose GPUs. Even NVIDIA is alarmed — it recently spent $20 billion acquiring Groq’s technology and team, a company specializing in high-speed inference chips. That move alone tells you: the fattest piece of its territory is being eyed.

So the real question isn’t whether NVIDIA is versatile. It’s whether AI inference turns out to be more like BTC or more like ETH. Can specialized chips beat it by an order of magnitude and shove NVIDIA off the richest ground — or is there something about inference that lets general-purpose GPUs hold on a while longer? I don’t have the answer. What I do know is that every current trend points to custom silicon closing in on inference fast — and the part of NVIDIA’s future that carries the highest hopes is sitting right on top of inference.

The Shovel-Seller Digs for Gold

There’s a business pattern in crypto I know well: mining hardware manufacturers almost always mine themselves. They sell machines and build their own mining farms — taking profit from both sides. And they mine with structural advantages: their machines cost less because they built them; each new chip generation gets run internally first to extract the cream of profits before “last-gen” models go on sale to outside miners. Same industry, vastly different economics — not competition on a level field, but an asymmetric advantage.

NVIDIA is running the same playbook now. Only the scale and complexity dwarf anything those mining hardware companies ever attempted.

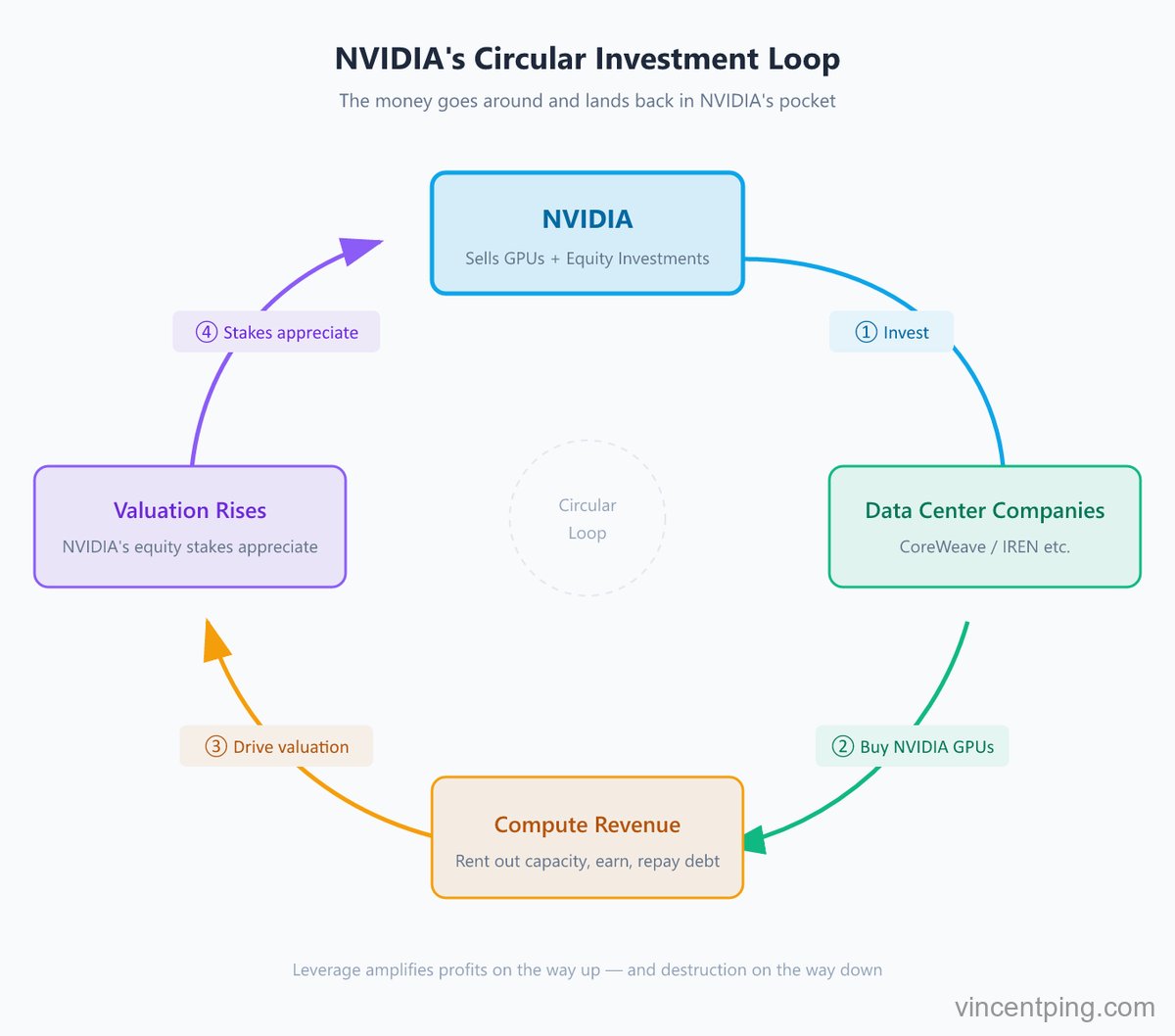

Its private equity investments went from roughly $3.4 billion a year ago to over $22 billion at the start of this year — more than a 6x increase. The money flows into AI infrastructure up and down the stack, and a significant portion goes to companies that buy its chips, or buy them indirectly through cloud providers. The loop is simple: NVIDIA invests money so these companies can afford to buy its GPUs. Those companies rent out the compute, earn revenue, service their debt, and their valuations rise — which makes NVIDIA’s equity stakes appreciate. The money goes around in a circle and comes back to NVIDIA’s pocket. Analysts have been blunt about it: these deals “fit squarely within the circular investment theme.” Jensen Huang isn’t hiding it either — at a conference this year he said NVIDIA “has truly become an infrastructure company, not just a GPU company.” The goal is to control the entire stack: networking, compute, software, data centers.

And the data center companies it invests in enjoy the same advantages as those mining hardware manufacturers who ran their own farms: they’re first in the supply queue, they get the latest generation cards, and pricing and allocation decisions sit in NVIDIA’s hands. The shovel-seller doesn’t just want to dig for gold — it digs with better shovels than anyone else can buy.

But the flip side of that advantage is risk. This entire structure is leveraged. Mining hardware companies building farms worked the same way — partnering with local operators in regions with cheap electricity, putting up machines while partners handled site, power, cooling, and connections. At the height of it, many were pledging their existing BTC — or even future BTC — as loan collateral. NVIDIA’s version: its investments lever up downstream companies’ debt, secured against future compute contracts. Add leverage, and the whole operation scales up and up.

When the market rises, leverage makes the wins spectacular — GPU sales profit on one side, equity appreciation on the other. But the other edge of the blade is always there. If those multi-billion-dollar compute contracts can’t be fulfilled on schedule, the chain unwinds bottom-up: the debt-laden companies default first, then the $22 billion in equity on NVIDIA’s books shrinks with them. In good times, leverage amplifies profits. In bad times, it amplifies destruction.

Old Players, New Table

If everything above is just “similar shapes,” there’s one thing where even the people haven’t changed.

Over the past two years, the crypto mining industry has collectively rebranded itself as AI data centers. Core Scientific, IREN, TeraWulf, Hut 8, Riot — these are all old mining names. Listed mining companies sold a record 30,000+ BTC in Q1 2026 — more than during the 2022 crash — liquidating core assets they’d been hoarding, just to fund their pivot into AI. Hut 8 said on its earnings call that Bitcoin is no longer the company’s “long-term strategic focus.”

But look closely at how they pivoted, and not all of them were pushed out by mining. A good number saw it coming early and left on their own terms — selling their crypto while prices were still high, betting that AI was worth more than mining. And their exit, in turn, pushed crypto prices down, squeezing the holdouts into selling at a loss just to survive. The early movers were shrewd. The late movers were desperate. But they all ended up at the same new table.

That rush toward whatever’s hottest — I know it too well. Every boom’s workforce comes from the last boom’s bust. This time, the bust is mining and the boom is AI. The table is new. The players are old. Even the urgency they bring is old.

And full circle: these rebranded old players end up right back in front of NVIDIA. In that circular investment loop I described earlier, the data center companies NVIDIA funds include their names — IREN and others were mining farms just yesterday. NVIDIA sells them cards on one side and invests money so they buy more cards on the other. And they are a crowd that just arrived from the last gold rush, chasing the wave. Every link in this chain radiates the same familiar heat — the same people, rushing toward the hottest thing, again.

A Pair of Glasses

I need to be clear about something, so I’m not misread: I am not bearish on AI.

Quite the opposite. I believe AI is this generation’s Industrial Revolution — call it the Information Revolution if you prefer. But that’s a completely separate matter from everything I’ve said above.

When the dot-com bubble burst in 2001, nobody could say the internet was useless. Email was in use then and is still in use today — never stopped for a single day. The internet genuinely changed the world. That didn’t stop the NASDAQ from collapsing that year, didn’t stop a wave of companies going to zero. The technology can be as real as it gets. The bubble pops anyway.

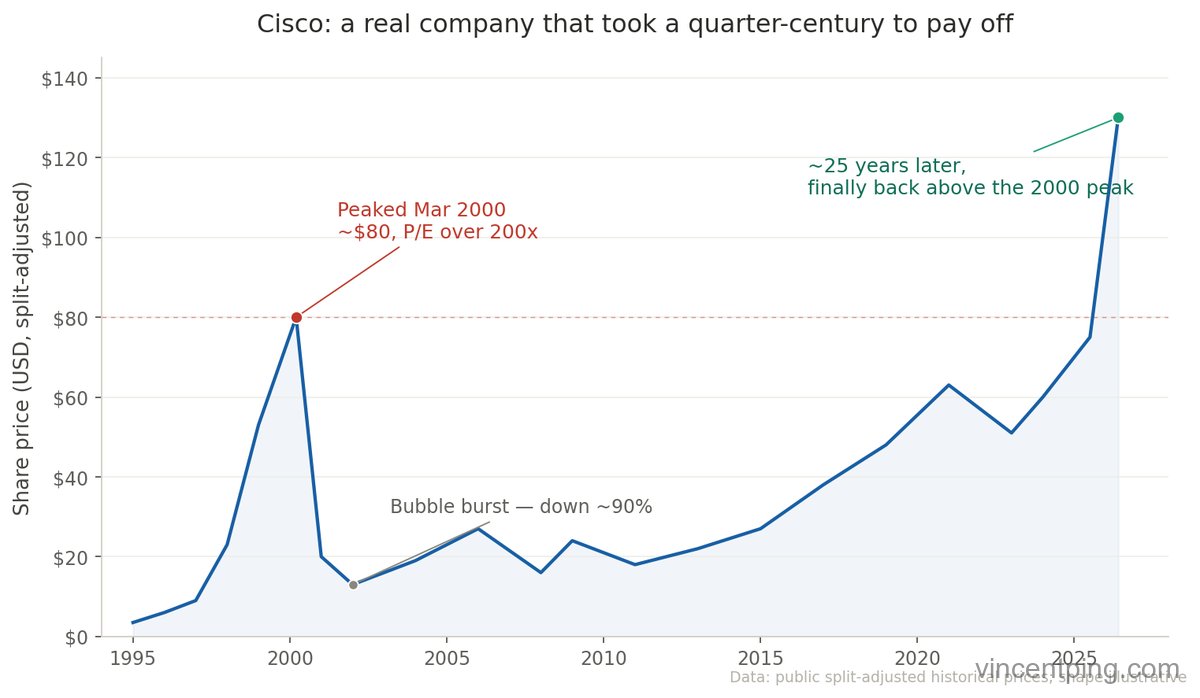

Within that bubble, one company’s story reads like a mirror today — Cisco. It sold “internet plumbing”: routers, switches, the backbone hardware of the entire internet. The narrative back then was word-for-word identical to today’s: nobody knows who wins at the application layer, but everyone has to buy Cisco. It became the world’s most valuable company then. P/E ratio above 200. Then the bubble burst, and its stock dropped nearly 90%. Note: Cisco wasn’t a fraud. It never went bankrupt. It remained profitable. Networking equipment is still essential today. But even a company that solid — its stock took twenty-five years to climb back to its 2000 peak. Meaning: even if you correctly called “the internet will change the world” and you correctly picked the hardest shovel-seller, buying at a price set by mania meant waiting a quarter century to break even.

Swap “Cisco” for “NVIDIA” and that sentence works almost unchanged. Same ecological niche — one sold network plumbing, the other sells compute. Same “nobody knows who wins, but everyone has to buy it” positioning. Same title of world’s most expensive company. I’m not saying NVIDIA is the next Cisco. History doesn’t repeat that simply. I’m saying: the Cisco mirror tells us that technology being real, the company being good, the product being essential — all three together still can’t prevent a price set by mania from spending two decades paying off.

Some will say that bubble at least left fiber optic cables in the ground, which got used later — a “good bubble.” Fair point, but it may not apply today. Even Morgan Stanley flagged the difference: fiber lasts twenty years. Today’s GPUs are obsolete in two or three. When the fiber bubble burst, the pipes stayed buried, waiting for the next wave. If these GPUs don’t earn back their cost within their lifespan, they leave nothing behind when they’re retired — just like my mining cards, which ended up sold as scrap for 2 RMB per kilogram.

That’s what those mining years really left me: a pair of glasses that lets me hold two things at once — that a thing can be real, useful, even world-changing, and at the same time be inflated by frenzy into an enormous bubble. So “AI is a genuine revolution,” however true, says nothing about whether NVIDIA’s price today makes sense. The truth of a technology and the fate of its price have always run as two separate lines.

The technology line, I can still read a bit. The price line — where it goes from here, I can’t call. I never called coin prices either; I didn’t step off at the top, the power bill pushed me off. Predicting was never my job. Setting down what I saw and what I made of it — that is.

This piece focused on NVIDIA alone. Where the profits actually land when all this money pours into AI — I follow that thread in the next one, The AI Business Through a Crypto Miner’s Eyes.

References

- SEC 2022 settlement with NVIDIA for failing to disclose mining’s material impact on gaming revenue ($5.5M): https://www.sec.gov/newsroom/press-releases/2022-79

- CNN reporting on the settlement (NVIDIA “omitted material information, was misleading”): https://www.cnn.com/2022/05/06/tech/nvidia-sec-settlement-crypto-mining

- Sequoia Capital’s David Cahn, “AI’s $600B Question” (estimating ~$600B annual revenue needed to justify current capex; his Dec 2025 update notes end-user revenue still “tens of billions/year” vs. “trillions in infra investment over five years”): https://www.sequoiacap.com/article/ais-600b-question/

- TrendForce data on custom AI chip share erosion vs. general-purpose GPU and shipment growth differential: https://www.spotedcrypto.com/hut-8-cipher-digital-ai-data-center-pivot-2026/

- Morgan Stanley comparing this AI capex cycle to the telecom bubble, noting GPU depreciation (2–3 years) vs. fiber (20+ years): https://medium.com/@truthbit.ai/the-2-trillion-question-can-ai-revenue-catch-up-to-capex-df8c5c3c52fb

- Ethereum’s Ethash memory-hard anti-ASIC design; BTC ASIC’s orders-of-magnitude advantage over GPUs (Wikipedia): https://en.wikipedia.org/wiki/Ethash

- CNBC: NVIDIA’s private equity investments grew from ~$3.39B to ~$22.25B in one year, covering the full AI infrastructure stack including chip customers (analyst: “fits squarely within circular investment theme”; includes IREN 5GW infrastructure deal): https://www.cnbc.com/2026/05/09/nvidia-embraces-ai-investor-topping-40-billion-in-equity-bets-2026.html

- Bloomberg: NVIDIA invested another $2B in CoreWeave in Jan 2026 (latest circular financing example): https://www.bloomberg.com/news/articles/2026-01-26/nvidia-invests-another-2-billion-in-coreweave-offers-new-chip

- Jensen Huang at Computex 2026: “NVIDIA has truly become an infrastructure company, not just a GPU company,” emphasizing full-stack infrastructure strategy: https://finance.yahoo.com/sectors/technology/articles/nvidia-become-infrastructure-company-jensen-003249580.html

Written in June 2026. All figures are publicly available estimates at the time of writing. Different sources use different methodologies; numbers will change over time. Verify against the latest primary disclosures before citing.